This weekend I did something I haven't done in a long time, I listened to "Moneytalk with Bob Brinker Host" live while driving to go windsurfing. I had read about how Brinker recommended selling the Vanguard GNMA fund (VFIIX) he recommended on the radio show for years to buy the Fidelity Floating Rate Income Fund (FFRHX) but had not heard him address this on the radio before today.

WARNING: FFRHX acts like a typical stock fund while VFIIX acts like a bond fund in your asset allocation.

This weekend a caller asked about this advice and mentioned his "financial advisor" recommended an annuity instead. Brinker then went on his typical warpath rant about how terrible annuities are and how the "financial advisor" may want a big commission. It was clear that after recommending the GNMA fund on the radio for years and years, you had to pay to read his Marketimer to see any more of his reasons for selling the GNMA fund to buy the Fidelity Floating Rate Income Fund that contains much of what some call "junk bonds."

It is not a surprise he wanted to sell the GNMA fund after it suffered major losses. For years, when callers asked about the interest rate risk in this fund, Brinker suggested they either

- Sell the fund and buy a CD ladder or other, similar investments with FDIC insurance. This is is what I did with most of my money in "fixed income." I also have money in individual TIPS bought directly from the US Treasury and ibonds, both investments that will never lose money if held to maturity.

- Place a mental stop loss on the GNMA position and sell when the NAV (net asset value) drops below this price.

Apparently, Brinker followed his own advice to sell GNMAs after they lost about a year or two's worth of interest and he placed the money in a new fund.

The new fund is very aggressive and should perform in-line with stocks. That is a TERRIBLE idea for anyone with a "balanced portfolio" where the whole idea of balance is diversification so the bonds go up when stocks go down. This fund lost 16.47% during the 2008 bear market while the GNMA fund went up about 8%.

WARNING: FFRHX acts like a typical stock fund while VFIIX acts like a bond fund in your asset allocation.

FFRHX Junk Bond Fund lost money in the bear market!!

GNMA Fund went up in 2008 bear market

This is what you want in a "balanced portfolio" to offset stock risk

If you don't want to suffer losses, you should buy CDs

If Brinker is recommending his subscribers buy this fund with money that was in GNMAs, beware that this is a very, very bullish change in his outlook..

- If he was so smart and good at market timing, whey didn't he switch out of GNMAs and into this fund in 2009?

- Is he taking calls about this fund on the radio show as a way to sell newsletters to those who lost money in the fund without telling them the fund behaves more like a stock than a typical bond fund?

- Brinker got bearish in 2009 by taking off "dollar cost average new money" to his "fully invested position at the very bottom... now at new record highs, he is recommending selling a typical, relatively safe bond fund to buy a fund that holds junk bonds and behaves like a stock fund? Another contrarian indicator?

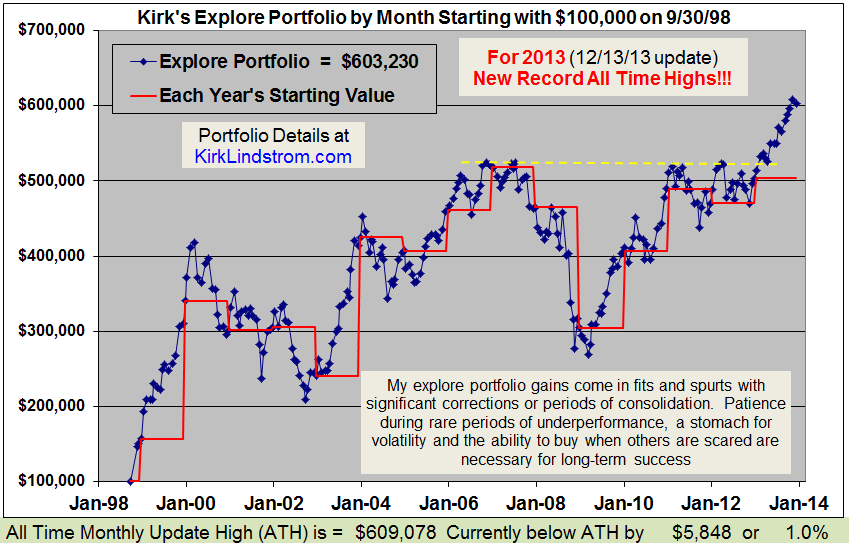

RECORD HIGH!!!

Long Term Results that Speak for ThemselvesSince 9/30/98 inception, "Kirk's Newsletter Explore Portfolio" is UP 450%vs. the S&P500 UP only 106% vs. NASDAQ UP only 101% (All through 6/30/13)

- Subscribe to my service NOW and get the July 2013 Issue for FREE! ! Your 1 year, 12 issue subscription will start with next month's issue.

- Get email alerts when I buy or sell securities for my explore portfolio

- "Auto Buy" and "Auto Sell" levels set ahead of time for target buy and sell levels for my securities. This allows you to place "limit orders" with your broker in advance so you can go about your business.

- All questions about what I write answered by Email. If what I write is not clear to you, just ask!

- Only $155 per year via PayPal & $150 if you send a check.

Charts and Price Quote for

and