WARNING! Bob Brinker's "Balanced" Model Portfolio Three is NOT balanced!

Brinker may show percentages that are 50% in equities and 50% in fixed income and often speaks of how this is to reduce risk during bear markets. I caution readers that the percentages Brinker recommends are not what he has in these portfolios. For example, this (repeated below) would lead you to think his "balanced" Model Portfolio III is half in stocks and half in fixed income, but if you look at the dollars he lists each month, he has the portfolio over two thirds in equities, not half!

- A balanced portfolio has half in stocks and half in fixed income that typically goes up when stocks go down

- Brinker's Model Portfolio 3 is over 2/3rds in stocks!

- Brinker's Model Portfolio 3 contains "risky" fixed income funds that have a positive correlation to the stock market. That is the "junk bonds" will typically lose value during a recession when stock prices also fall.

Brinker may show percentages that are 50% in equities and 50% in fixed income and often speaks of how this is to reduce risk during bear markets. I caution readers that the percentages Brinker recommends are not what he has in these portfolios. For example, this (repeated below) would lead you to think his "balanced" Model Portfolio III is half in stocks and half in fixed income, but if you look at the dollars he lists each month, he has the portfolio over two thirds in equities, not half!

Here is Bob Brinker's Model Portfolio III, which is a 50% equities/50% fixed income portfolio, "best suited to investors nearing or already enjoying a retirement lifestyle". As of March 4, 2014 Marketimer newsletter:

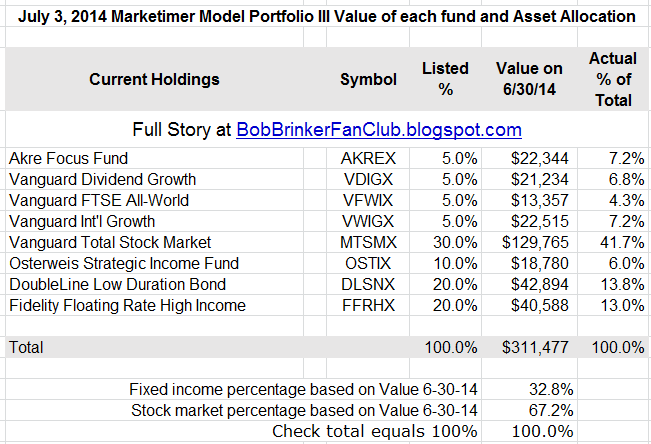

Akre Focus Fund (AKREX): 5%Vanguard Dividend Growth (VDIGX): 5%Vanguard FTSE All-World ex US Index (VFWIX): 5%Vanguard International Growth (VWIGX): 5%Vanguard Total Stock Market (VTSMX): 30%Osterweis Strategic Income Fund (OSTIX): 10%DoubleLine Low Duration Bond (DLSNX): 20%Fidelity Floating Rate High Income (FFRHX): 20%

Stock fund vs Bond Funds

Brinker doesn't rebalance his portfolios to 50% stocks. As a result, when the markets are going up, he can report higher returns than competitors who rebalance.

Here is the composition of Model Portfolio 3 just before the biggest bear market since the great depression:

Another result that he doesn't talk about is these portfolios give up far more to the downside from their peaks during bear markets. |

| click images to see full size |

One of my readers sent me this a few days ago showing the totals for the portfolios and the percentages Brinker shows. I added a column at the right that calculates the ACTUAL portfolio allocation to each fund.

That is the portfolios with two thirds in stocks have far more risk than "typical" balanced portfolios like the ones I recommend in my newsletters. See

- "Kirk's Two Investment Letters - Which is Best for You?"

ALL the funds in my core portfolios are at Vanguard but I give ETF substitutions for those who want to use Fidelity, Schwab, etc.... I rebalance about once a year so the costs are tiny and you can avoid those by using the free to trade funds at those fund families, also listed in the newsletter as alternatives.

Another factor is taxes from switching funds, which Brinker does often and I almost never do except for eliminating total bond fund until rates normalize to reduce risk.

Brinker switches his portfolios at any time. So unless your money is 100% tax deferred it is very difficult to keep your portfolios up to date and get anything approximating the returns he advertises. You may have to open accounts at multiple firms and good luck balancing across them.

ReplyDeleteHere was portfolio I in July of 2008

15% Baron Partners

05% Dodge & Cox International

15% Meridian Growth Fund

15% Rydex OTC Fund

05% Vanguard International

45% Vanguard Total Stock Market

Compare that to what you posted now...

10% Akre focus fund

10% Vanguard small cap

10% Vanguard dividend growth

10% Vanguard FTSE All-world

10% Vanguard International growth

50%Vanguard total stock market

That is a substantial difference in the same portfolio not even 6 years later - 4 funds are different so you would have incurred capital gain/lose taxes and then had t deal with transferring of accounts etc and then the issue of rebalancing across custodians etc. And then to do what, implement the fantasy known as market timing?

For example Brinker market times and has made several horrendous calls that are not factored into his posted returns. Besides his infamous QQQ debacle he jumped out of the market in 87 and did not get back in until after the market had substantially recovered. In other words he sold near the bottom and bought back in after a large run up.

My advice - don’t waste you time with Bob Brinker.

Are these funds for retired people or the clueless?

ReplyDeleteOsterweis Strategic Income Fund (OSTIX): 10%

DoubleLine Low Duration Bond (DLSNX): 20%

Fidelity Floating Rate High Income (FFRHX): 20%

Retirees following his 50% fixed income/50% equities approach currently have their 50% fixed income allocated in the 3 mutual funds above. I don't think many Bogleheads would approve of having 20% of a portfolio in a Floating Rate (bank loan) fund. 85% of the bonds in the Fidelity Floating Rate High Income fund are below investment grade.

About 82% of the bonds in the Osterweis Strategic Income Fund are below investment grade, garnering 10% of his recommended retiree portfolio.

About 21% of the DoubleLine Low Duration Bond fund is in below investment grade bonds.

Where's the downside protection here? The other 50% of the portfolio is in equities. What happens to the entire portfolio in a bear market?

What purpose is this fixed income allocation of the total portfolio serving?

What is the risk level of the total portfolio if 50% is in equities and the 50% fixed income portion has such a high percentage in below investment grade fixed income?

And this is the portfolio for retirees????